Although buzzwords such as “investment factors,” “factor funds,” “smart/strategic beta” have recently gained popularity, factor investing was pioneered back in the 1960s. This era gave birth to many modern finance theories, including the seminal Capital Asset Pricing Model (CAPM). Factor investing, a methodical approach to choosing investments, has seen significant evolution since then.

CAPM and Future Advancements

Factor investing traces its origins to the 1960s, particularly the Capital Asset Pricing Model (CAPM). Developed by academics like Sharpe, Lintner, and Mossin, CAPM emphasised the role of market returns in explaining stock returns by claiming that a stock's expected return depends on its beta, a measure of its responsiveness to market movements.

Despite its contributions, CAPM faced challenges. CAPM explained a small portion of the returns, largely due to its many theoretical assumptions. CAPM’s failure to explain various market phenomena, such as the Value Effect, Size Effect, and Momentum Effect, motivated academics to develop more sophisticated multi-factor models which explain risk and return based on factors other than beta.

Expanding the Paradigm with Fama and French

In response to CAPM's limitations, Fama and French introduced their seminal three-factor model in 1992. Going beyond market risk, it considered size and value factors as well. These developments can be considered as the official inception of multi-factor investing. Later, in 2015, they further refined the model with two additional factors: profitability and investment. This refinement allows for a broader understanding of expected asset returns, considering not just the stock’s systematic risk (beta) but also size, value, profitability, and investment characteristics.

Growing Factors and Competing Models

Factor investing continued to evolve with the addition of momentum in 1997 by Carhart and the introduction of alternative models like the Hou, Xue, and Zhang q-factor model.

Factor investing is a rapidly evolving domain marked by the continuous introduction of new factor models and parameters. This expansion brings forth both opportunities and challenges.

Navigating the diverse array of factor parameters demands a discerning approach. The critical need is to distinguish genuine sources of excess returns from those potentially arising from data mining. This consideration holds utmost significance for researchers and practitioners, underscoring the need for rigorous methodologies and meticulous analysis.

Integration of Academic Research into Real-world Portfolio Management

Despite its academic success, factor investing remained largely theoretical throughout the 1980s and early 1990s. During this time asset managers were intrigued but hesitant in the face of implementation challenges. Data was scarce, and transaction costs for constructing portfolios based on these factors were considerably high.

By the mid-1990s, technology and data availability began to catch up. Asset managers like Dimensional Fund Advisors (DFA), led by David Booth and Rex Sinquefield, and influenced by Eugene Fama, were among the first to bring factor investing to life. DFA launched the US Small Cap Value Portfolio in 1993, one of the first funds to explicitly incorporate size and value factors. This successful incorporation of academic findings into action provided an early validation of factor-based investing.

The 2000s marked the creation of factor-specific indexes. Recognizing the need for transparency and replicability, index providers like MSCI, S&P Dow Jones, and FTSE Russell began designing indexes that targeted specific factors, such as value, momentum, and low volatility.

At the same time, financial institutions began to embrace factor investing. BlackRock, AQR Capital Management, and other industry giants launched multi-factor funds, combining factors like value, momentum, quality, and low volatility into a single strategy. The narrative shifted from "why factor investing?" to "how can we use it better?"

Later in 2014, Vanguard launched its Vanguard Value ETF (VTV) and Vanguard Small-Cap Value ETF (VBR), further democratizing factor-based investing by offering low-cost access to value and size factors.

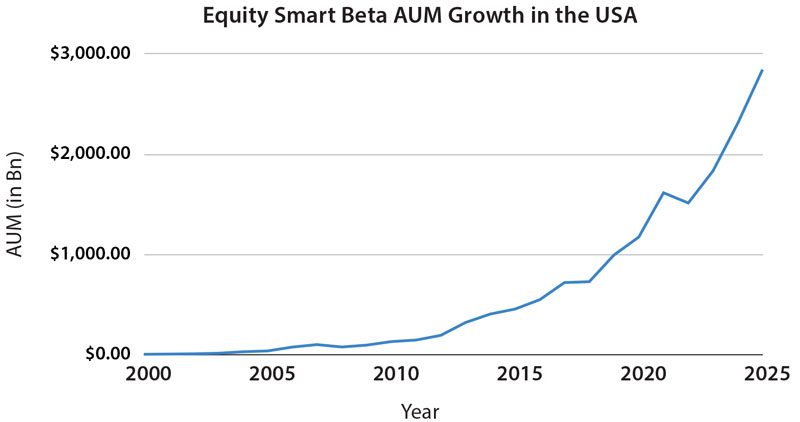

The integration of academic research into real-world portfolio management has significantly influenced the growth of Smart Beta ETFs, as depicted in the chart and table. The chart illustrates the steady rise in the Assets Under Management (AUM) of equity Smart Beta ETFs in the U.S., with notable acceleration post-2010. This growth aligns with the broader acceptance of factor investing strategies by both institutional and retail investors.

The table further reinforces this growth trajectory. Over the last 15 years, Smart Beta ETFs have experienced a cumulative AUM increase of 22.99%, while since 2000, the growth stands at an impressive 36.65%. This trend signifies a maturing market where investors increasingly recognize the benefits of systematic, rules-based investing approaches.

Source: Bloomberg Intelligence. Data as of 31st December 2025

| Time Period |

AUM Growth |

| Last 3 Years |

23.44% |

| Last 5 Years |

19.41% |

| Last 10 Years |

20.18% |

| Last 15 Years |

22.99% |

| Since 2000 |

36.65% |

Source: Bloomberg Intelligence. Data as of 31st December 2025

Impact of Technology and Future Developments

Today, factor investing has become increasingly popular, with practitioners utilising and developing factor-based products due to their transparent and systematic rules and relatively low costs. The next few years will be interesting as we see how factor investing continues to evolve.

Technological and computational advancements have profoundly impacted factor investing, enhancing the capacity to process and analyse vast datasets, often referred to as big data, and identify complex patterns and relationships that drive asset returns. Machine learning and artificial intelligence (AI) have further revolutionised this field, allowing for the examination of non-linear relationships and the potential discovery of new, subtle factors. These technologies facilitate the development of sophisticated, data-driven investment strategies which also benefit risk management by improving the modelling of factor exposures and correlations. However, these technological advances also introduce new challenges, such as the risk of overfitting and the need for clear interpretability of complex models.

Factor investing has been pivotal in reshaping asset pricing and portfolio management. Originating from the market-centric view of CAPM, it has evolved into a multifactor perspective, notably influenced by Fama-French models. While successful in explaining market anomalies and aiding portfolio diversification, challenges persist—factor timing, market crowding, and the integration of non-financial data, such as ESG factors, pose complexities. The surge in factors and parameters raises concerns about data-snooping and the stability of factor premiums. Nevertheless, factor investing remains a vibrant area of research and practice, adapting to a changing financial landscape. The future will likely witness continued adaptation, leveraging technological advancements and data analysis to refine and potentially redefine critical factors for investment success. In this complex landscape, the connection between theoretical rigour and practical application remains crucial for investment success.

| Factors used in various factor models |

| |

Market Beta |

Value |

Momentum |

Size |

Profitability/ Quality |

Investment |

| Fama French 3 Factor (1993) |

YES |

YES |

- |

YES |

- |

- |

| Carhart Momentum (1997) Addition to 3 Factor Model |

YES |

YES |

YES |

YES |

- |

- |

| Fama French 5 Factor (2015) with Momentum |

YES |

YES |

YES |

YES |

YES |

YES |

| Hou et. al. Q-factor (2015) |

YES |

- |

- |

YES |

YES |

YES |